The Extended Credit Facility (ECF) provides financial support to help Ghana address balance of payments challenges and promote economic stability.

To heal the sick economy

To enable Ghana pay her debt

To grow the economy & care for the poor

Comprehensive Guide to Ghana's Economic Recovery Framework

The ECF for Ghana outlined 5 key prior actions necessary for the approval of the program. These actions were to ensure that Ghana was taking the necessary steps to stabilize the economy and meet the IMF's requirements.

2023 Budget Approval: Ghana had to pass a budget that emphasized revenue enhancement and expenditure rationalizations.

Revenue Mobilization: Implementation of measures to improve tax collection and broaden the tax base.

Agreement with External Creditors: Reaching agreements with external creditors to restructure debt, addressing severe financing constraints unsustainable public debt.

Implementing steps to enhance transparency and efficiency in the public spending through better audit and control mechanisms e.g. publication of Audit Report on Covid-19 Expenditure

Financial Sector Stability: Measures aimed at strengthening banking regulations and improving financial sector oversight to ensure stability

Utility Tariffs: Adjusting utility tariffs to ensure cost recovery and reduce the financial burden on the government

These are specific, measurable targets that Ghana must achieve to continue receiving funds from the IMF

Targets set to reduce the fiscal deficit.

Specific levels of reserves Ghana must maintain.

Targets to bring inflation back to single digit.

Specific reduction targets for the debt-to-GDP ratio.

These are comprehensive reforms aimed at addressing systemic issues and enhancing economic stability

Reforms to improve tax collection and broaden the tax base.

Measures to enhance transparency and efficiency in public spending.

Reforms to address inefficiencies and vulnerabilities in these critical sectors.

Measures to strengthen banking regulations and improve financial sector oversight.

These are benchmarks that, while not binding, are used to monitor Ghana's progress

Ensuring that budget adjustments do not disproportionately affect vulnerable populations, maintaining or increasing spending on social programs e.g. LEAP, School Feeding Program & Capitation Grant.

Encouraging policies to boost private investment and economic growth.

Maintaining specific levels of debt service to avoid defaults.

Comprehensive analysis of Ghana\'s key economic performance metrics from Q1 2021 to Q1 2024. This interactive dashboard presents GDP growth, nominal GDP, interest rates, inflation rates, and exchange rate trends, providing insights into the country\'s economic trajectory and monetary policy effectiveness.

| Quarter | GDP Growth (%) | Nominal GDP (Billion GHC) | Interest Rate (%) | Inflation (%) | Exchange Rate (GHC/USD) |

|---|---|---|---|---|---|

| 2021 Q1 | - | 114.02 | 14.50 | 10.30 | 5.70 |

| 2021 Q2 | -13.28 | 102.95 | 13.50 | 7.80 | 5.80 |

| 2021 Q3 | 8.42 | 114.59 | 13.50 | 9.70 | 5.90 |

| 2021 Q4 | 9.98 | 130.14 | 14.50 | 12.60 | 6.00 |

| 2022 Q1 | 3.92 | 142.79 | 17.00 | 15.70 | 7.10 |

| 2022 Q2 | 4.60 | 131.99 | 19.00 | 29.80 | 7.60 |

| 2022 Q3 | 2.97 | 153.92 | 24.50 | 37.20 | 9.60 |

| 2022 Q4 | 3.83 | 185.64 | 27.00 | 54.10 | 8.60 |

| 2023 Q1 | 3.15 | 212.07 | 29.50 | 52.20 | 11.00 |

| 2023 Q2 | 2.55 | 189.86 | 30.00 | 42.50 | 11.20 |

| 2023 Q3 | 2.16 | 206.61 | 30.00 | 38.10 | 11.50 |

| 2023 Q4 | 3.79 | 233.09 | 30.00 | 23.20 | 12.10 |

| 2024 Q1 | 4.69 | 266.68 | 29.00 | 23.20 | 12.90 |

The First Review of Ghana's Extended Credit Facility (ECF), published by the International Monetary Fund (IMF) in September 2023, assessed the country's economic performance and implementation of reforms under the program. This comprehensive evaluation examined Ghana's performance across Quantitative Performance Criteria (QPCs), Indicative Targets (ITs), and Structural Benchmarks (SBs).

Binding and measurable targets that must be met by the government to maintain program compliance.

| Indicator | Target | Performance |

|---|---|---|

| Fiscal Primary Balance | Achieve positive primary balance | Achieved: Strong fiscal consolidation efforts |

| International Reserves (Commitment Basis) | Increase reserve accumulation | Exceeded: Improved by over 4 percentage points of GDP |

| International Reserves (Cash Basis) | Reduce fiscal deficit impact | Achieved: Significant improvement through fiscal measures |

| Non-Concessional Borrowing | Limit external borrowing | Achieved: Borrowing limits maintained |

| Net Domestic Financing | Control domestic borrowing | Achieved: Financing kept within agreed limits |

Supplementary targets that guide policy decisions and monitor program implementation.

| Indicator | Target | Performance |

|---|---|---|

| Social Protection Spending | Increase spending on social programs | Achieved: Safety net programs expanded |

| Inflation Control | Reduce inflation rate | Achieved: Declined from 54% to 23% |

| Domestic Arrears Clearance | Reduce outstanding arrears | In Progress: Partial achievement, challenges remain |

Specific reform commitments designed to improve long-term economic performance and governance.

| Indicator | Target | Performance |

|---|---|---|

| Tax Reform | Broaden tax base and enhance revenue collection | Achieved: Revenue improvements implemented |

| Public Financial Management Reform | Strengthen PFM systems | In Progress: Improvements ongoing |

| Energy Sector Reforms | Reduce inefficiencies and fiscal risks | In Progress: Additional reforms needed |

Ghana successfully met most Quantitative Performance Criteria, particularly excelling in fiscal consolidation and reserve accumulation. The fiscal primary balance showed marked improvement due to strong reform efforts, while international reserves exceeded targets, enhancing macroeconomic stability. Debt management remained under control within agreed parameters.

Performance on Indicative Targets was largely positive. Social protection spending increased to protect vulnerable groups during the adjustment period. Inflation dropped significantly from 54% to 23% through effective monetary policy. However, domestic arrears clearance remained challenging, requiring continued attention.

Structural reforms showed mixed progress. Tax reforms and revenue collection improvements were successfully implemented. Public financial management reforms advanced but required continued effort. Energy sector reforms, while showing some progress, needed additional work to address long-term fiscal sustainability concerns.

GDP growth for 2023 was revised to 1.5%, reflecting challenges from energy production constraints, elevated inflation, and fiscal adjustment measures. Inflation began declining from its December 2022 peak of 54% to 40.1% by August 2023, though it remained elevated.

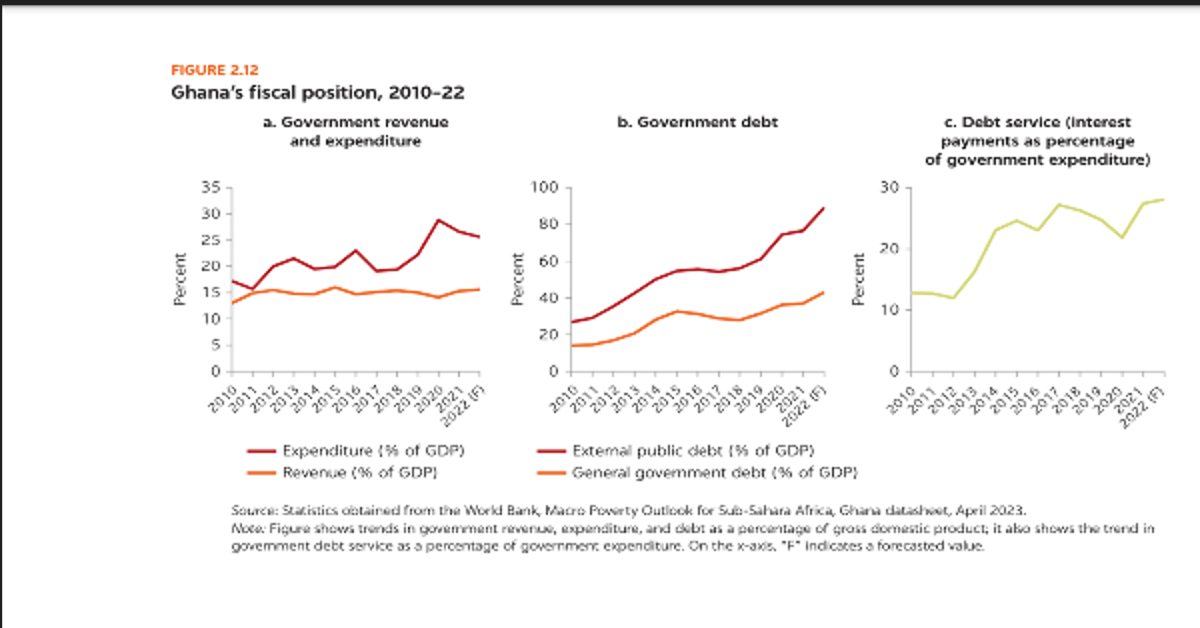

The fiscal deficit was targeted to narrow to 1.5% of GDP in 2023 from 6.9% in 2022. Government revenues increased through improved tax collection and enhanced fiscal measures, supporting consolidation efforts.

Ghana continued negotiations with creditors to restructure public debt and restore sustainability. Domestic debt restructuring made progress, while external debt restructuring discussions advanced with international partners.

The current account deficit was projected to narrow to 2.4% of GDP in 2023, supported by strong remittances and improved export performance. Foreign exchange reserves stood at $2.2 billion, equivalent to approximately 1.1 months of import cover.

The Second Review of Ghana's Extended Credit Facility represented a critical assessment of the country's economic recovery program. This comprehensive evaluation examined Ghana's progress across multiple performance indicators, structural reforms, and macroeconomic targets designed to restore fiscal stability and promote sustainable economic growth.

Ghana's performance under the Extended Credit Facility demonstrated significant progress in key areas while highlighting ongoing challenges requiring continued attention.

Ghana successfully met most Quantitative Performance Criteria and made substantial progress on structural benchmarks, demonstrating strong commitment to the reform program despite challenging economic conditions.

Mandatory targets forming the backbone of the IMF program, measuring Ghana's fiscal discipline and macroeconomic stability.

Ghana achieved significant improvement in its fiscal primary balance, with a surplus targeted at 0.5% of GDP in 2024. This represented a remarkable turnaround from previous deficits, reflecting the government's commitment to fiscal consolidation and responsible spending practices.

The government successfully met targets for non-oil revenue collection, signaling substantial progress in improving tax administration and broadening the revenue base. Enhanced collection mechanisms and improved compliance drove this achievement.

Ghana exceeded targets for building international reserves, contributing to a significantly stronger external sector position. This achievement enhanced the country's capacity to manage external shocks and maintain exchange rate stability.

While public debt levels remained elevated, substantial progress was made in restructuring existing obligations and implementing improved debt management practices. The debt restructuring process gained significant momentum during this period.

| Performance Criteria | Target Status | Achievement Level |

|---|---|---|

| Fiscal Primary Balance | 0.5% of GDP surplus | ✓ Target Met |

| Non-Oil Revenue | Enhanced collection targets | ✓ Target Met |

| International Reserves | Accumulation targets | ✓ Target Exceeded |

| Debt Management | Restructuring progress | ✓ Substantial Progress |

Supplementary targets guiding policy implementation and ensuring balanced economic development across all sectors.

Ghana successfully increased social protection expenditures to mitigate the impact of economic reforms on vulnerable populations. Programs were expanded to provide crucial support during the adjustment period, ensuring social stability.

The government maintained spending within strict budgetary limits, significantly reducing fiscal pressures and improving overall macroeconomic stability through disciplined expenditure management and enhanced fiscal oversight.

The Bank of Ghana continued implementing tight monetary policies, which proved instrumental in dramatically reducing inflation from 54% in 2022 to 23% by end-2023, creating a more stable economic environment.

The Bank of Ghana's tight monetary stance achieved remarkable results, with inflation declining by more than half from peak levels, creating a more stable environment for businesses and households while supporting economic recovery.

Long-term structural reforms designed to strengthen institutional capacity and improve economic governance frameworks.

Ghana made significant strides in strengthening domestic revenue collection through comprehensive tax reforms and substantial improvements in public financial management systems and processes, enhancing fiscal transparency.

Structural reforms enhanced transparency in debt management practices, including implementation of improved tracking systems for debt sustainability and enhanced reporting mechanisms to international partners and stakeholders.

While progress was made in these critical sectors, additional reforms were identified as necessary to address persistent inefficiencies and potential fiscal risks that could impact long-term economic stability.

The Second Review demonstrated Ghana's strong commitment to the IMF program, with the country successfully meeting most quantitative performance criteria and making substantial progress on structural reforms. The achievement of fiscal targets, coupled with improved revenue collection and enhanced monetary policy effectiveness, positioned Ghana favorably for continued program success.

Ghana's fiscal consolidation efforts yielded impressive results, with the primary balance moving toward surplus territory. The dramatic reduction in inflation from 54% to 23% represented one of the most significant achievements, while the strengthening of international reserves provided crucial external stability during a challenging global environment.

While overall performance was strong, the energy and cocoa sectors required ongoing attention to address structural inefficiencies and enhance productivity. Continued debt management efforts and sustained fiscal discipline remained critical for maintaining program momentum and achieving long-term economic stability and growth.

The International Monetary Fund staff team, led by Mission Chief Mr. Stéphane Roudet, completed its mission in Ghana for the third review of the country's three-year Extended Credit Facility program. The mission assessed progress on economic reforms and macroeconomic performance.

A staff-level agreement was reached on the third review of Ghana's economic program under the Extended Credit Facility arrangement. Pending IMF Management approval and Executive Board consideration, Ghana gained access to SDR 269.1 million (approximately US$360 million), increasing total disbursements under the arrangement to SDR 1,441 million (US$1.92 billion) since May 2023.

Economic growth in the first half of 2024 exceeded expectations, driven primarily by the mining, construction, and information and communication technology sectors. Growth broadened across other sectors in the second quarter, demonstrating increased economic resilience.

While inflation continued to decline, drought conditions in the northern regions posed risks to agricultural output and could place upward pressure on food prices, requiring careful monitoring and policy responses.

Ghana remained on track to achieve a primary surplus of 0.5% of GDP in 2024, despite fiscal pressures from drought conditions and ongoing challenges in the energy sector. This achievement reflected strong fiscal discipline and effective policy implementation.

The Bank of Ghana maintained a tight monetary policy stance to support continued inflation reduction and maintain macroeconomic stability.

Significant progress was made on key structural reforms, although some areas experienced implementation delays that required attention.

Discussions focused on enhancing energy sector sustainability and transparency, strengthening revenue collection mechanisms, improving expenditure controls, and bolstering social protection programs to protect vulnerable populations during the economic transition.

Ghana achieved significant milestones in its comprehensive public debt restructuring efforts:

The external sector showed improvement in 2024, driven by strong gold exports, moderate oil exports, and higher remittance inflows from the diaspora.

International reserves surpassed program targets, providing enhanced buffer against external shocks.

Financial sector stability remained intact, with continued progress in bank recapitalization efforts and increased profitability across the banking sector.

The IMF team held productive meetings with Finance Minister Dr. Mohammed Amin Adam, Bank of Ghana Governor Dr. Ernest Addison, senior government officials, and other key stakeholders in the economic reform process.

The team expressed appreciation for the Ghanaian authorities' continued cooperation and constructive engagement throughout the review process.

The Fourth Review under Ghana's Extended Credit Facility, completed in July 2025, marked a significant milestone following the general elections. The new administration demonstrated strong commitment to the reform program despite facing considerable fiscal challenges inherited from the previous government.

Ghana's economic performance in 2024 exceeded expectations, with real GDP growing 5.7% and continuing with robust growth of 5.3% in Q1 2025. While inflation remained elevated at 23.8% at end-2024 (above program targets), it showed encouraging declines to 18.4% by May 2025 and further to 13.7% in June. The external sector strengthened significantly with a current account surplus of 1.1% of GDP in 2024, and international reserves reached three months of import coverage.

The primary balance deteriorated significantly to a deficit of 3.3% of GDP versus the targeted surplus of 0.5%, representing a major fiscal slippage that threatened program objectives and required immediate corrective action.

Net accumulation of payables reached approximately 2.6% of GDP, with most occurring outside the Government Integrated Financial Management Information System (GIFMIS). This included GHS 67.5 billion in gross accumulation, with GHS 49.2 billion outside formal financial systems, mainly from infrastructure projects and electoral spending pressures.

The new administration launched a thorough audit of 2024 commitments and arrears to fully understand the fiscal situation inherited from the previous administration and develop appropriate corrective measures.

A new 2025 Budget was enacted targeting an ambitious primary surplus of 1.5% of GDP, demonstrating strong commitment to fiscal consolidation and restoring program credibility through decisive action.

The administration amended the Public Financial Management and Public Procurement Acts, enhanced the fiscal responsibility framework with a debt anchor, while the Bank of Ghana increased the policy rate by 100 basis points to support disinflation efforts.

Ghana made substantial progress in its debt restructuring efforts with the completion of domestic debt restructuring in 2023, followed by the successful Eurobond exchange in October 2024. A Memorandum of Understanding with the Official Creditors Committee was signed in January 2025, with remaining commercial creditors representing less than 5% of total debt. These achievements led to credit rating upgrades by major international rating agencies.

The sector resumed quarterly tariff adjustments to improve cost recovery, though challenges remain with over US$2 billion in payables to Independent Power Producers, requiring continued attention and structured resolution.

Production recovery continued with farmgate prices set at GHS 49,600 per metric ton, supporting farmer incomes and providing production incentives while maintaining the sector's contribution to export earnings.

A new Gold Board (GoldBod) was established with US$279 million in capital to enhance gold sector development, improve value addition, and strengthen revenue generation from the mining sector.

The National Investment Bank was successfully recapitalized with an adopted restructuring plan to restore its viability. Most banks remained on track to meet the 13% Capital Adequacy Ratio requirement by end-2025. The Bank of Ghana enhanced its open market operations to improve monetary policy transmission and financial market functioning.

Economic growth is projected to moderate to 4.0% in 2025 before returning to 5.0% by 2027 as structural reforms take effect. The inflation target of 8±2% is expected to be achieved by mid-2026 through continued tight monetary policy. The fourth review was completed on July 7, 2025, with a US$367 million disbursement approved, bringing total disbursements under the program to US$2.3 billion.

Get comprehensive details on Ghana's fourth review performance and future economic prospects

Fifth review